1. Initiation of tapering and interest rate hike in 2022

In December 2020, the FED reiterated that it would continue to buy bonds until the economy had made “substantial” progress towards stable 2% inflation and a healthy labor market.

However, due to the mounting risk of losing control over inflation, the FED has announced to phase out the bond purchasing program and possibly increase the interest rate in 2022.

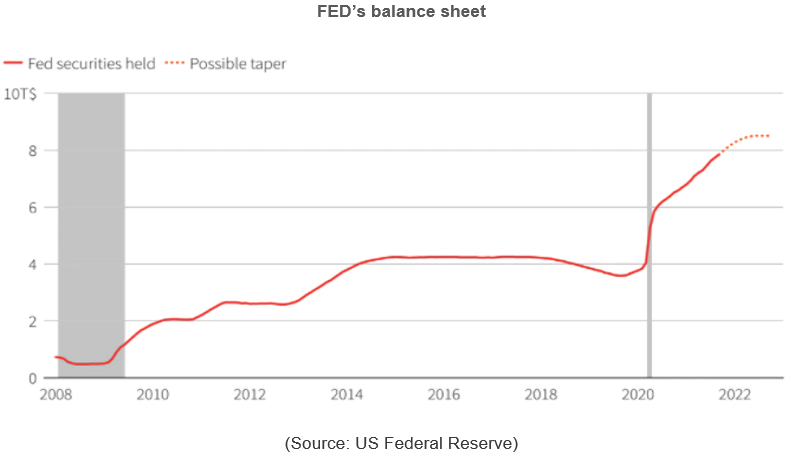

In early December 2021, the Federal Reserve announced that it would begin to wind down the bond-buying program designed to prop up the economy during the pandemic. The FED said it would slow down its monthly asset purchases, starting from later this month, at a pace of $15 billion per month and end the tapering in June 2022.

However, concerning that the big rising in inflation is not temporary, the market still believes that the FED will double the pace of tapering to $30 billion per month, starting in January 2022 and wrapping up in March 2022.

Bond purchasing program

In line with the expectation of the market, on 15 December 2021, FED announced that it would end its pandemic-era bond purchases in March, paving the way for three interest rate hikes by the end of 2022, as policymakers voiced concerns over persistently high inflation against a backdrop of a steady recovery in the labor market.

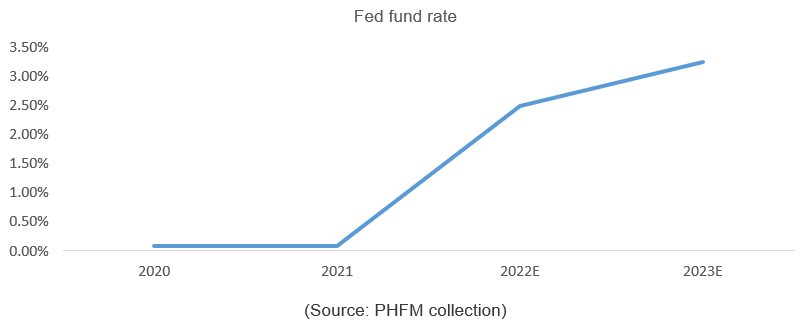

Interest rate hike

In the meeting on May 2022, the FOMC raised the FED fund rate by 50bps after the inflation data of the US in recent months showed that it was not temporary. Previously, there had been no consensus for a rate hike in 2022.

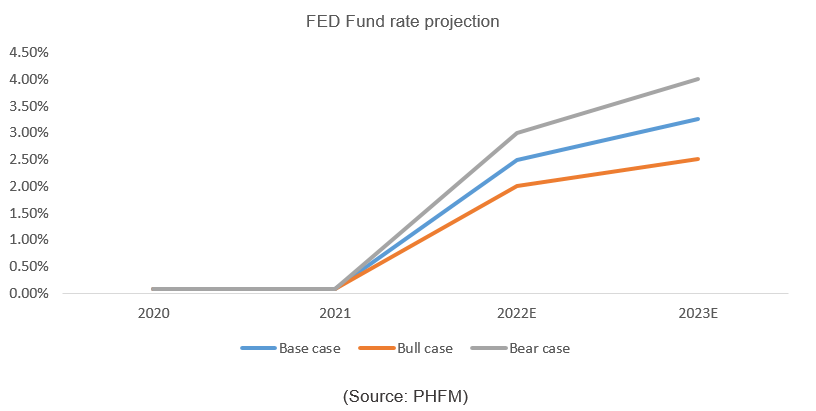

The market expects that FED will continue to hike the interest rate to 2.5%-3% by the end of 2022, and the rate should be steady in 2023.

The rapid increase of the interest rate is mainly to combat the inflationary pressure as FED kept its long-term goal of the “2% inflation.”

2. A lesson from the previous taper tantrum in emerging countries

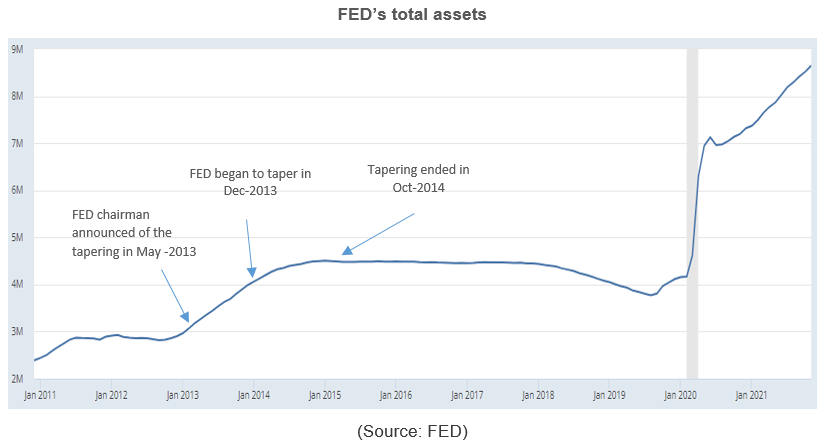

On 22 May 2013, Federal Reserve Chair Ben Bernanke announced that the FED would start tapering asset purchases, but no specific date has been appointed.

On 18 December 2013, the FED announced the beginning of tapering. It steadily reduced monthly bond purchases throughout 2014, winding them down entirely in late October.

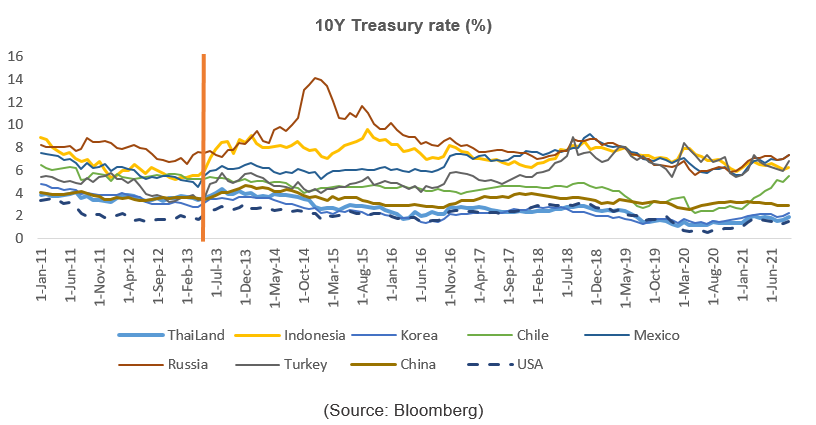

The US 10Y T-bond yield had seen a nearly 1.5 percentage point increase from 30/04/2013 to 31/12/2013. As a result, the T-bond in other countries, including the emerging market, started to follow the rally of the US T-bond.

Among the emerging countries, the T-bond yield of Russia (+7.5 percentage points), Indonesia (+3.3 percentage points), and Turkey (+2.5 percentage points) were the highest jumper. Meanwhile, the others only saw a slight increase of 0.5 to 1.5 percentage points in the T-bond yield.

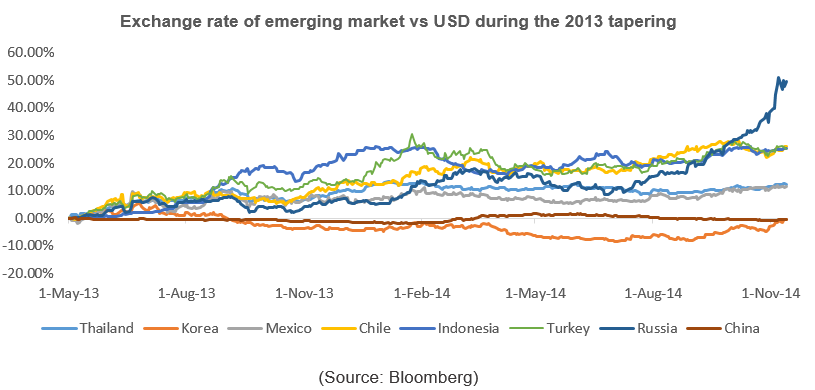

Once again, Russia, Indonesia, and Turkey had witnessed the biggest loss in their currency against the US dollar, while the stable bond-yield countries had seen a steadiness in their exchange rate.

So, what happened to the Emerging market? Investor panic triggered a sell-off in bonds, causing Treasury yields to surge. As a result, emerging markets suffered sharp capital outflows and currency depreciation, forcing central banks in Emerging market to hike interest rates to protect their capital accounts.

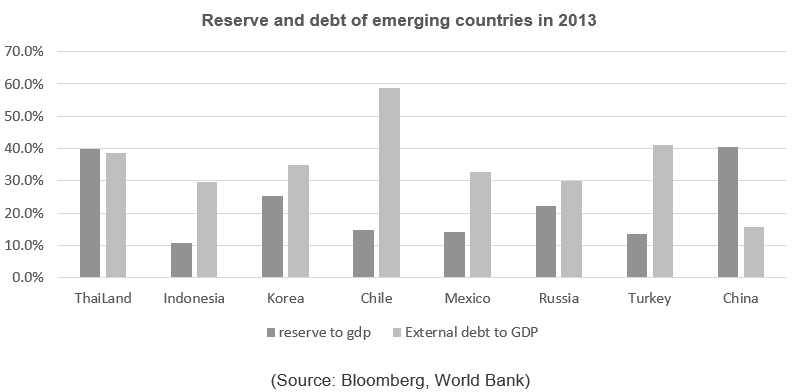

To guard against instability arising from shifting capital flows, central banks in emerging-market economies hold reserves—liquid, foreign-currency-denominated assets. These reserves provide foreign-currency liquidity to domestic borrowers when it is hard to obtain from foreign lenders, thus enabling domestic borrowers to finance current deficits and roll over maturing debt.

We see that emerging countries with high Reserve Ratio and low external Debt to GDP will relatively have a stronger buffer against the shocks that are brought by the taper tantrum.

Most of the listed emerging countries with a Reserve to GDP below 20% are more exposed to the risk of devaluation of the currency and an interest rate hike.

Thailand and Russia are the exceptions due to their unstable political condition. For Russia, which was impacted by the sanctions of Europe and a significant drop in the oil price from 2014 to 2015, its interest rates and the exchange rate have to face unfavorable conditions. While in Thailand, the Bath was mainly affected by the political crisis – the Coup d’état.

China and Korea are the biggest winners. Thanks to their high reserve ratio and stable macro and political conditions, those countries had remained a stable in both T-bond yield and foreign exchange.

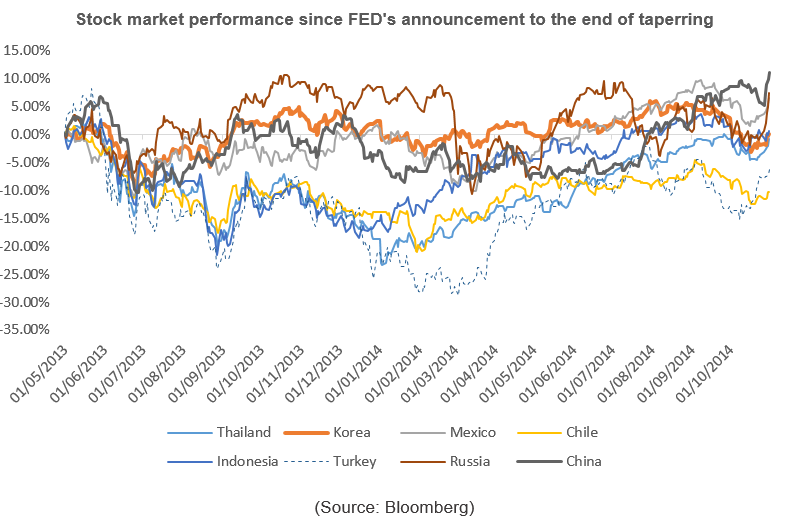

The stock market in the tapering year was not favorable. However, as we mentioned, the countries with strong buffer had not seen a significant volatility in the stock performance.

3. What could happen to Vietnam in the 2022 tapering?

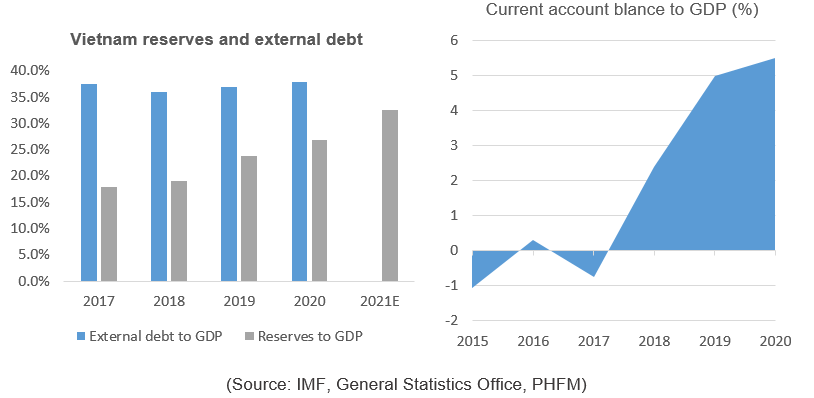

In our opinion, Vietnam is in a good position for the 2022 tapering. First of all, Vietnam’s Reserve Ratio has been strengthened in recent years thanks to an impressive FDIs inflow, trade balance surplus, and a massive remittance. According to the IMF, Vietnam’s reserves could reach US114 bn, equivalent to 32.6% of 2021 GDP.

At the same time, Vietnam’s foreign currency debt remained stable at around 38%, thanks to the economy’s solid growth.

We expect that with a high Foreign Reserves accumulation in the last couple of years and a stable macro and political condition, Vietnam will withstand the tapering in 2022. We expect the Vietnam Dong to remain stable and should not see a big devaluation.

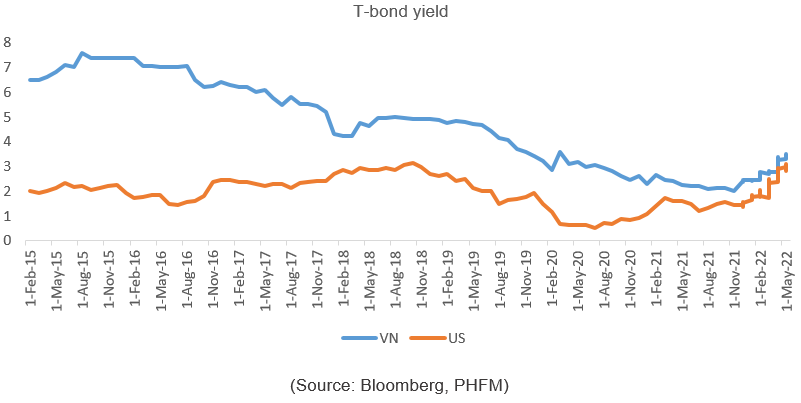

Both T-bond yields of the US and Vietnam were not volatile during the tapering procedure from FED at the end of 2021.

However, after the hike in the interest rate in May 2022 and the possible of a four-to-five rate hike, the T-bond yield has seen a strong rally in recent months.

The hike in the interest rate and capital outflow could temporarily impact Vietnamese stock market in terms of devaluation. However, backed by the economy’s positive outlook and the expectation of upgrading to the MSCI-emerging market, we believe that the Vietnam stock market will continue to enjoy a solid growth.

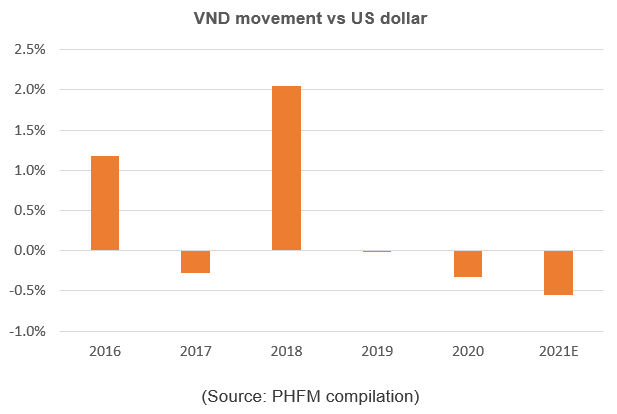

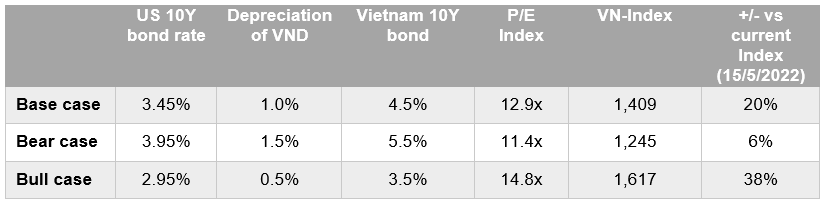

With careful preparation from the government, we expect that the Dong will only slightly depreciate from 0.5% to 1.5% in the upcoming years. Using the interest rate parity, we forecast the 10Y bond yield of Vietnam should be at 4.5% in the base case scenario, equivalent to the rise of 2.1 percentage points in 2022.

The stock market could see a devaluation due to the rise of the interest rate. Given the GDP growth rate of 6% in 2022 and the earnings growth of the listed companies could be at 15%YoY. Thus, VN-Index target should be at 1,409 in our projection.

Base case FED fund rate as end of 2022 is at 2.5%

Bear case FED fund rate as end of 2022 is at 3.0%

Bull case FED fund rate as end of 2022 is at 2.0%