In November 2021, the COP26 international climate conference took place in Glasgow, where countries worldwide have come together to issue a solid commitment to cut down fossil fuel consumption significantly, then secure global net-zero carbon by mid-century. But now, six months later, no large nation has come forward with a bolder climate plan, and most of them, especially the Europe, are confronting the worst energy crisis in decades due to the lack of oil & gas and other fossil fuel supply from Russia resulting from the war in Ukraine, and the subsequent sanctions spiraling up.

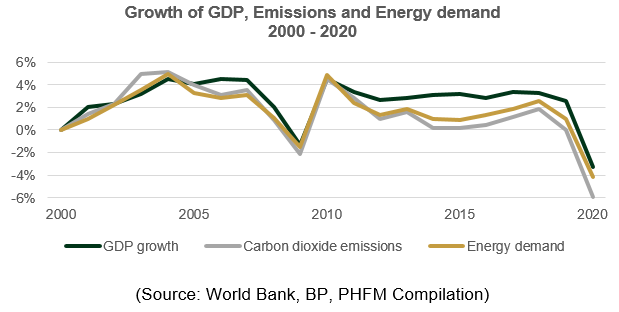

The challenging situation implicitly indicates the world’s heavy dependence on fossil fuels, especially oil & gas, for energy to run the economy. Indeed, the demand for them was enlarging over the years alongside the GDP growth and carbon emissions, just before the severe disruption caused by the coronavirus pandemic outbreak worldwide in 2020.

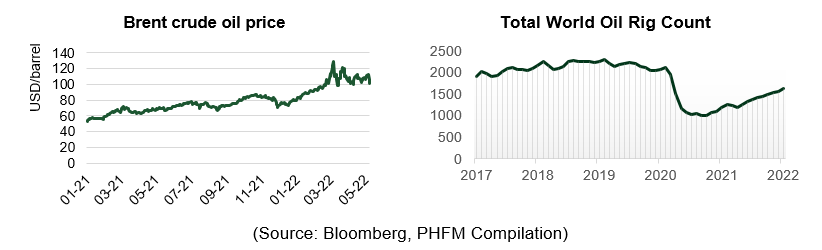

Immediately after the vaccine rollouts, the economy rebounded rapidly alongside the demand for oil & gas. The crude oil prices, at times, surged to a 13-year high of over USD139/barrel as the supply restoration could not meet the rapid rebound of global oil demand despite the restart of many oil rigs worldwide. While whole markets are facing the escalating geopolitical tension in Europe, the prices only somewhat cooled down when the US & other G7 countries released their strategic oil reserves, and China increasingly imposed its zero-covid policy recently. However, these have only short-term effects.

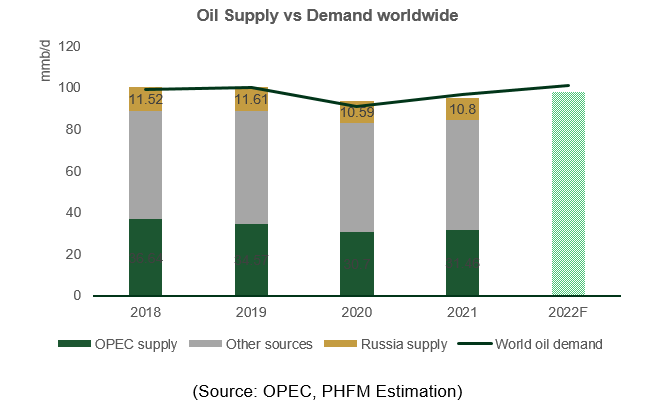

Demand is outstripping supply globally amid the armed conflict in Europe

By the end of April 2022, the prices increased by 1.35% (MoM) and remained at a high level of USD109.3 per barrel, driven by the persistent supply outages since the Ukraine war occurred. In response to major energy-consuming nations, OPEC+ (including Russia) has agreed to proceed with the modest oil increase by more than 432 thousand barrels per day from May 2022. However, there are concerns that members of the organization will not be able to promptly achieve their committed output levels, and the amount gained is also unable to offset the disruption caused by Eastern Europe tension so far. Indeed, the current geopolitical threats between Russia and Ukraine are becoming more severe and going on fiercely.

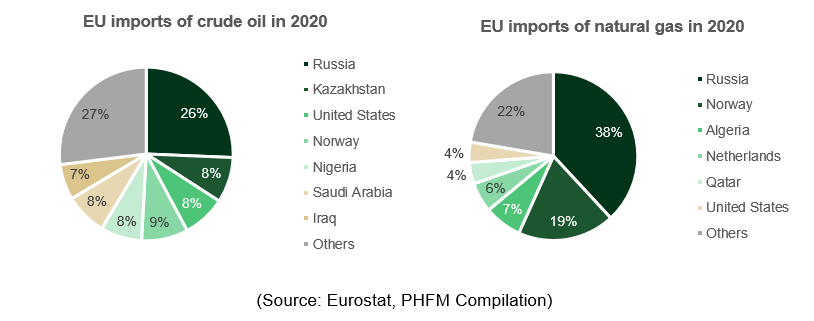

Consequently, many severe sanctions would be imposed on Russia, including expelling the country from the SWIFT Banking system and delaying Nord Stream 2 project. The circumstance will undoubtedly cease the oil & gas supply from Eurasia, then lift the prices worldwide. Furthermore, Russia is the largest among oil & gas suppliers globally and the EU, accounting for 26% and 38% of EU imports of crude oil and natural gas, respectively. It would be much more challenging to fulfill the potential supply shortage resulting from the sanctions in upcoming periods, even if the US and allies are releasing their strategic oil reserves. Therefore, we expect the prices will remain high for the long term.

Domestic supply tension keeps oil and gas prices high and reinforces a positive outlook

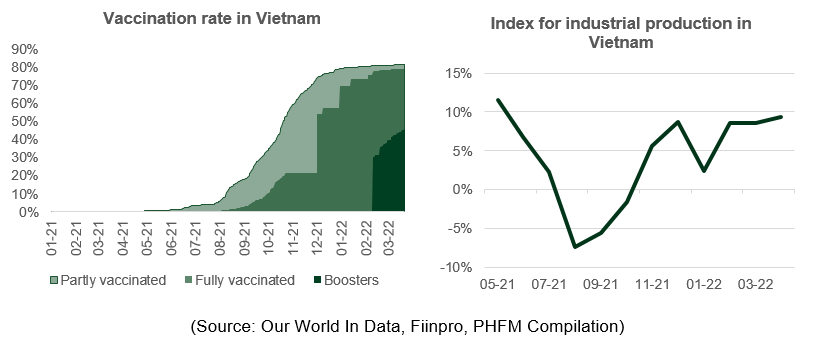

Since 2021, there has been a strong recovery of the national economy and the oil & gas industry from collapse thanks to high-speed vaccination and the removal of social distancing measures, which later provoked the bounce-back of manufacturing and transportation activities, inevitably consuming most of the gas and petroleum supply. The observed rebound in sales price and volume is adequately reflected in the companies’ performance in 2021.

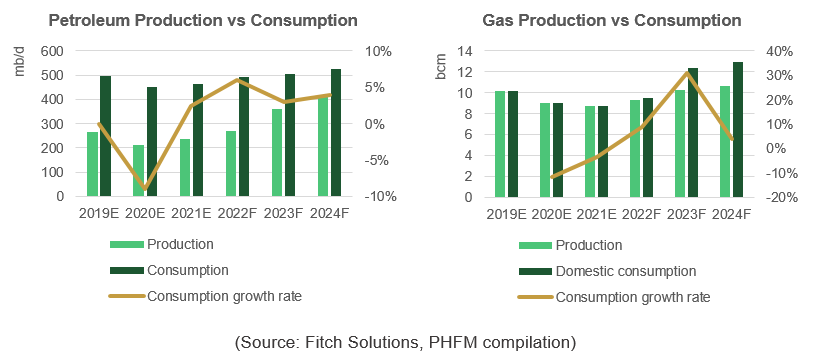

In Vietnam, the supply of crude oil and natural gas would be falling as the capacity of many fields is descending over the current years, and the development of many new projects suffers from severe obstacles in terms of policy and geopolitics. In contrast, the demand for petroleum, liquefied petroleum gas, and, especially, natural gas is expected to increase by 3%p.a, 10.5%p.a, and 14%p.a, respectively. Moreover, the government will shift the gas-fired power in the power mix of Vietnam to realize the decarbonization target in the vision for 2030 and 2045.

The domestic petroleum prices are under high pressure of increment following the surge in oil prices worldwide and the production disruption of the Nghi Son refinery due to financial issues. Despite the maximum operation of the only two refineries, Binh Son and Nghi Son, Vietnam still confronts an extensive deficit in supply and must rely on the imports to meet the increasing demand at present and in many upcoming years. It also means that the country would suffer from the fluctuation in international prices. Accordingly, the RON92 gasoline has increased significantly (by 29%) since the beginning of 2022, and so do other petroleum products.

LNG import is a solution for energy security in the long term

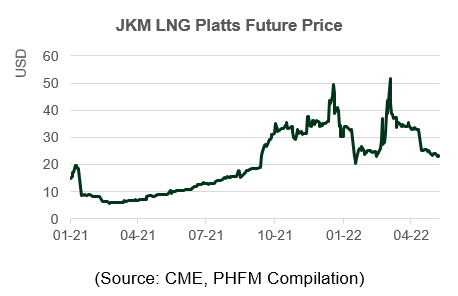

Vietnam plans to import LNG (Liquidated Natural Gas) for the first time in 2022 and sees this as a solution for lowering carbon emissions and ensuring national energy security in the long term. However, the global supply of LNG is tight, and most of the volumes of big producers such as Qatar are locked into long-term contracts mostly to Asian buyers, especially Japan and Korea. Therefore, we expect that the plan to use LNG in Vietnam will be postponed in the short term due to the supply shortage and the spike in LNG prices lately.

The first LNG project – LNG Thi Vai in Vung Tau Province, will be completed in 2022-2023, will supply two LNG-fired power plants, Nhon Trach 3 and 4 (1500MW), which are under implementation. Besides, PVGas (GAS) also set another milestone when it signed the Joint Venture Agreement with AES Corporation to develop the LNG Son My project to supply Son My Thermal Power Complex (4250MW). LNG Son My, coming into operation in 2025, alongside with LNG Thi Vai and many other projects, will shape Vietnam’s energy future.

The bright prospect of the oil & gas industry comes when the world and Vietnam face a potential energy shortage to meet the increasingly high demand for recovering manufacturing and fueling new growth. It would be promising in several years until renewable energy achieves breakthrough developments. Therefore, we anticipate the companies in the industry to benefit substantially from the positive outlook. The ones in the Petrochemical (oil refinery) and Gas sectors would be two major focuses because of the persistent supply deficit and the shift to gas-fired power determined by the government to realize the decarbonization target in coming years.