Vietnam and the “Net-Zero” Transition

At the 26th International Conference on Climate Change (COP26) in 2021, Vietnam committed to achieving net-zero emissions (Net-Zero). “On its part, despite being a developing country that started industrialization only over three decades ago, Viet Nam will capitalize on its advantage in renewable energy and take stronger measures to reduce greenhouse gas emissions. To this end, we will make use of our domestic resources, along with the cooperation and support of the international community, especially from the developed countries, in terms of finance and technology, including through mechanisms under the Paris Agreement, to achieve net-zero emissions by 2050.” – a speech from Vietnamese Prime Minister, Pham Minh Chinh at COP26.

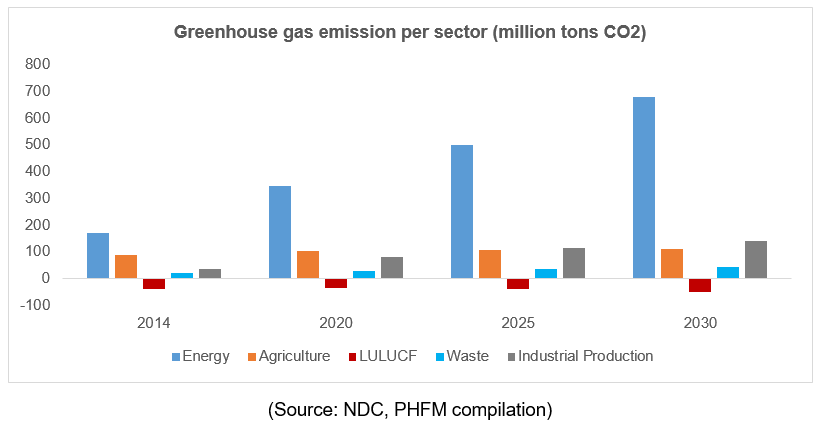

There are five sectors by the classification of activities of absorbing and releasing greenhouse gas (GHG): (1) Energy (including transportation), (2) Agriculture, (3) Industrial Production, (4) Waste, and (5) Land Use, Land-Use Change, and Forestry (LULUCF). Only the LULUCF sector is the GHG reducing sector that can only reduce about 10% of the total emission amount. The other four sectors are the releasing sectors, in which the energy sector is the biggest GHG emission source.

The LULUCF sector may reduce the higher emission amount in the future, but it cannot absorb all the emission amount. Forest is the main CO2 absorption sector in Vietnam, currently covering around 14.6 million ha area with a coverage ratio of 42%. There are less opportunities to increase the forest area in the future due to limitations. Thus, Vietnam needs a huge effort to achieve the target of Net-Zero.

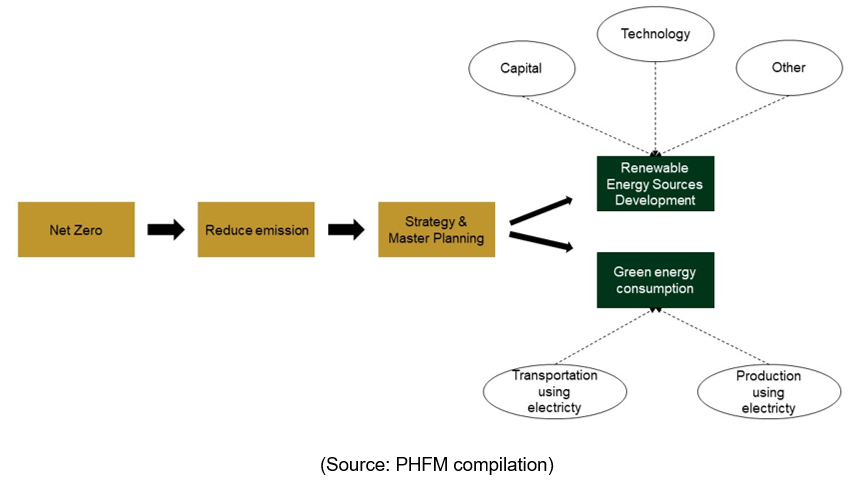

To reach Net-Zero, Vietnam needs to reduce the emission and increase the absorption. However, the economic and social development requires a huge demand for energy for industrial production, mining, and manufacturing. Thus, through the first effort, Vietnam focuses on decreasing the emission of the energy sector. Vietnam has started changing its power source capacity by increasing the “green” energy source. To develop renewable energy (RE) sources fast, Vietnam introduced many strategies and development plans to encourage RE sources development. At the same time, other economic and social sectors are encouraged to use the RE.

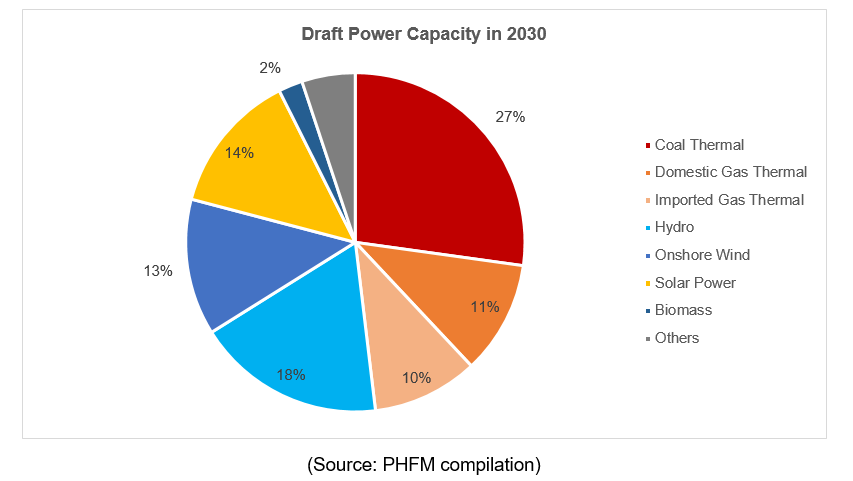

Focusing on decreasing the emission from the energy sector is the main target in the future. Vietnam’s Government has many policies encouraging the RE source. According to the current Draft of Power Development Plan VIII (PDP8), in the base case, the total capacity will reach 138 thousand MW by 2030 and 234 thousand MW by 2045. PDP8 ceases developing coal thermal power sources and requires wind power development, especially offshore wind power. The RE source accounts for 29% of the total power capacity in 2030, while wind power accounts for 13%, solar power accounts for 14% and biomass power accounts for 2%.

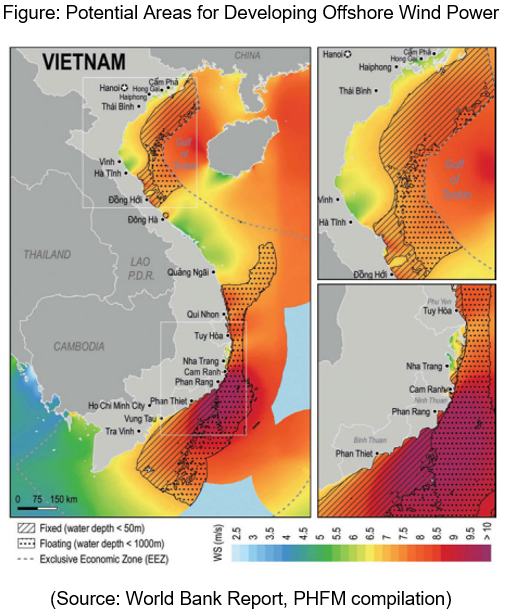

Thanks to its long coastline and many shallow areas, Vietnam has a huge wind power potential compared to other countries. Wind power is more stable than solar power. Offshore wind power is considered a long-term solution for meeting the system’s demand. On the other hand, solar power is not stable when the weather does not support it. Following to Offshore Wind Roadmap for Vietnam Report of the World Bank, the offshore wind capacity could meet 30% of the total capacity in 2050. By the end of 31 October 2021, Vietnam has 88 operating wind power projects with a capacity of 4.2GW.

Renewable Energy Trends and Listed Companies

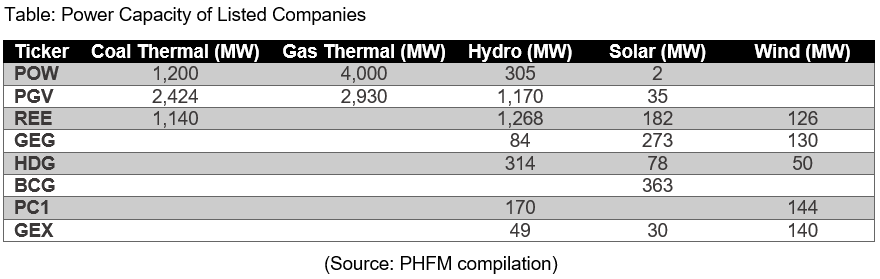

Many listed companies are developing renewable energy, but all big State-owned Enterprises (SOEs) power companies are not necessarily participating in developing new energy. For example, Genco 3 (HOSE: PGV) and PVPower (HOSE: POW) did not actively develop the RE sources since they are developing in thermal power and hydropower sources. Besides GEG, whose main business is only in electricity production, the other power companies have their main business activities in different industries. For example, REE has M&E services and real estate development business besides developing RE sources, Ha Do Group (HOSE: HDG) also has its main revenue from real estate development. Private companies have some advantages in the shareholder structure and capital raising (bond issuance) for developing projects.

The table below is the list of some companies’ capacities. There are two notes about the data in the table. Firstly, the data includes all capacities of parents, subsidiaries, and affiliates. REE and PGV both own Thac Ba Hydro Power (HOSE: TBC), Ninh Binh Thermal (HNX: NBP), and Vinh Son Song Hinh Hydro Power (HOSE: VSH). We add the whole number of capacities to the total without adjusting the ownership percentage. Secondly, solar power is installed as MWp, which we convert into MW.

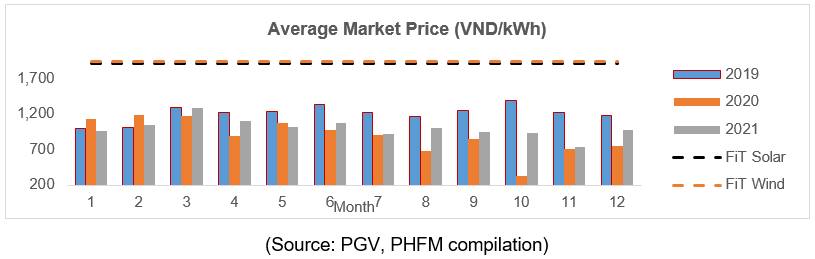

In our opinion, one of the reasons that SOEs do not actively develop the RE sources is the price. The deadline to complete the project and operate for having the preferential price FiT is quite urgent. FiT prices for the RE projects are 9.35 cents/kWh and 8.38 cents/kWh for solar power projects and 9.8 cents/kWh and 8.5 cents/kWh for wind power projects. These FiT prices are higher from 37% to 60% compared to the highest monthly price in 2019 – 2021. Investment in RE development is relatively high since the capital for 1MW wind power is around 2 million USD. If the sales price is not high and the demand is not guaranteed, would take a long time to reach the breakeven point, and the IRR of the project is not high. Unable to meet the completion deadline could cause trouble for SOEs.

Approximately 84 wind power plants with a power capacity of 4,000 MW could not meet the deadline for completion set before 01/11/2021 to enjoy the FiT price. Because these projects cannot run the plants at the market price, they are still waiting to operate when having the preferential rate.

Bright Outlook for The Power Sector

Tailwinds for the power sector will support the bright outlook. There are two catalysts for the power sector in the future. They are (1) the higher power market price and (2) the renewable energy development trend.

Potential Higher Power Market Price in The Future

Shortly, manufacturing companies in Vietnam can buy power directly from power suppliers. In May 2021, Samsung Vietnam wanted to participate in the direct purchase of pilot projects (DPPA – Direct Power Purchase Agreement) from available projects in the market. At the beginning of December 2021, LEGO Group (Denmark) signed the Memorandum of Understanding (MOU) about building a factory in Binh Duong – this factory will be the first carbon-neutral factory of the Group.

DPPA regulation will attract many big international companies which commit to using “green” energy in manufacturing. However, the official DPPA regulation is still in the drafting stage. According to the Electricity Regulatory Authority of Vietnam (ERAV), big customers using electricity from a voltage of 22kV or higher can negotiate the price and the output through the contract. The scale of the DPPA piloting phase will not exceed 1,000MW.

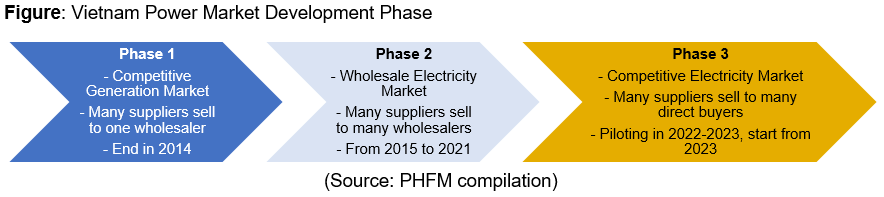

According to Vietnam’s electricity market development roadmap, 2022 is a prerequisite year to implement the competitive market in 2023. The competitive market will allow households to buy electricity directly from retailers. Firstly, the market will be piloted to allow large energy consumers to sign contracts with renewable energy suppliers. Then, the customer base of renewable energy will expand by adopting energy-heavy individuals (voltage level 110 kV) to buy power from the spot market directly. Finally, smaller retail customers can buy from retailers.

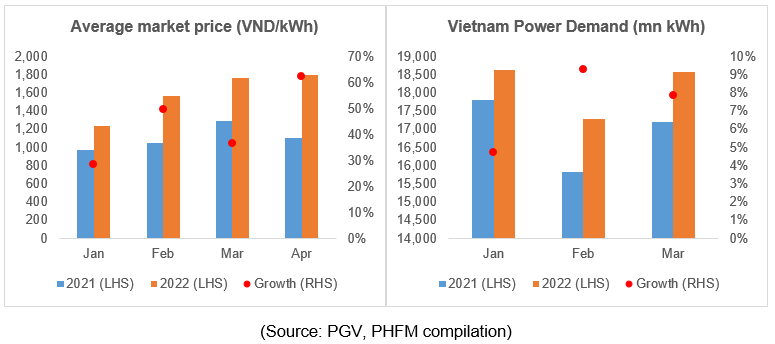

In phase 3 of the market, the power price could have a high growth because of the high price of the RE power plants. It will benefit companies that have good cost management and low debt level. The power market price in 2022 has increased, and the average power market price in 2022 will be higher than in 2021. The price increase in 2022 came from 2 main reasons: (1) The strong recovery from the production sector and especially the hospitality sector; (2) Thermal power is prioritized to mobilize in the year, which makes the price higher because of the high input price such as gas.

Renewable Energy Development

Decarbonization is the trend, and a huge capital allocation for the “net-zero” transition is happening globally. Vietnam is not out of this trend because there is active development in electric vehicle development and renewable energy.

This trend will benefit early-entrant power companies in the market. Specifically, we believe that companies, that (1) have the FiT price, (2) operate efficiently, and (3) are capable of developing projects quickly, will have the potential to grow in the long term. Completing the project early and having the preferential price will guarantee the investment return of the project, which also creates a cash flow for new projects. An efficient operation will also create an advantage when participating in the competitive market. Finally, raising capital quickly to develop the new project will support the company’s long-term growth.